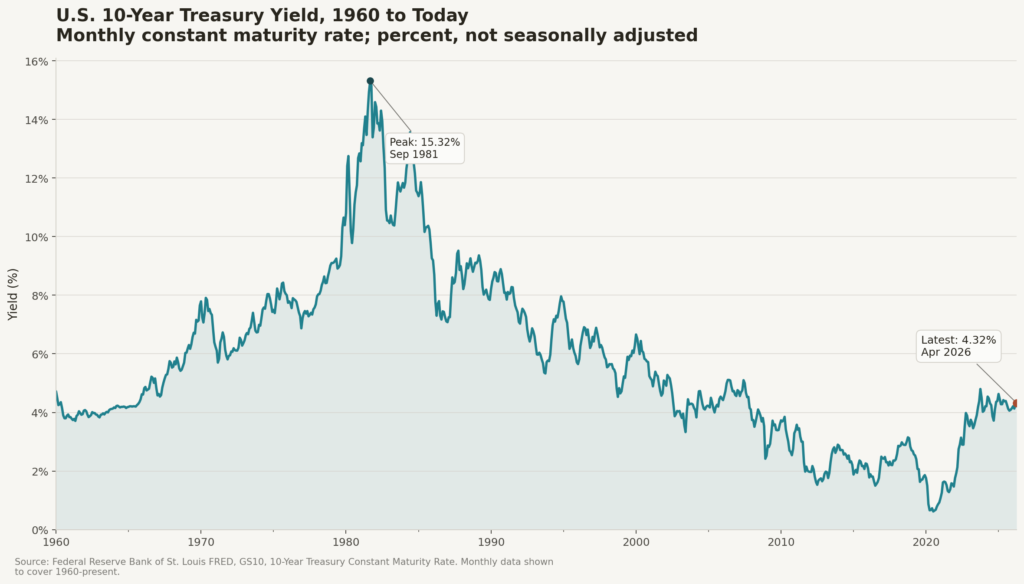

Bond investors are starting to ask what to do if yields keep rising, as rates are now well above their 2020 lows. If yields continue to drift upward, it raises the possibility of a prolonged bear market in bonds as bond prices move down as yields move up. We saw the opposite from 1980 to 2020, when ten-year yields fell from 15% to below 1% over multiple decades. Bonds delivered excellent returns during that period and, for long stretches, outperformed U.S. stocks.

Since 2020, yields have climbed back to roughly 4.45%.

Will they keep rising? Maybe, but just because they were at 15% doesn’t mean they’re going there again. Anchoring to past levels is a poor way to invest. But yields don’t need to revisit 15% for bonds to struggle, and persistent deficits could push them higher from here.

You can be forgiven for rolling your eyes at deficit warnings. They’ve been around since Reagan’s 1980’s budgets and haven’t helped investors as a timing tool. That doesn’t mean deficits don’t matter—even MMT proponents agree—it just means that no one can tell you when they will.

Deficit Fears

Last July in The Deficit, I explained that while the numbers are too big to ignore, deficits are a poor timing tool. What matters more is the deficit relative to GDP and that economists view 3% as sustainable. Today, we’re closer to 6% and DOGE didn’t fix that and tariffs won’t. That doesn’t tell us that yields will move sharply higher. They could remain rangebound, as they largely have over the past few years, even if that range is drifting upward.

What’s concerning is that we’re running these deficits in good economic times. In past downturns, like 2008–09 and the pandemic, deficits expanded sharply to absorb the shock, but from a much lower starting point than today’s roughly 100% debt-to-GDP. By contrast, we would enter the next downturn with roughly 100% debt-to-GDP and already elevated deficits, leaving less room to respond without risking pressure on rates or market confidence, meaning the next recession could be harder to fight or more likely to trigger a fiscal or financial crisis, especially when it’s clear that we’re collectively unwilling to bring revenue and spending levels closer to equilibrium.

Bond Portfolio Action Plan

So what should investors do?

If rising rates are a concern, one practical adjustment is to lean shorter in your bond portfolio.

Short- and intermediate-term bonds fall less when rates rise, and as they mature, you can reinvest at higher yields.

You don’t have to move entirely into ultra-short or cash-like positions, but trimming longer maturities and shifting toward the 1–5 year range can reduce rate sensitivity while maintaining income. Higher yields also mean higher expected returns for bond investors who can tolerate some volatility and reinvest as bonds mature.

With individual bonds, this is straightforward—you know when each bond matures and when you can reinvest.

With bond funds and ETFs, you don’t have a maturity date, so duration becomes the key metric. Duration estimates how sensitive a portfolio is to rate changes (a duration of 5 implies roughly a 5% decline for a 1% rise in rates) and how quickly it adjusts to a new rate environment. Durations under 3 years are considered short, 3–6 years are intermediate, and anything longer introduces meaningful interest rate risk. If rising yields are a concern, that’s the dial to evaluate and adjust.

Conclusion

You don’t need a view on where rates are headed to act. If yields rise, longer-duration bonds will feel it. If they don’t, you’ll still have a portfolio aligned with today’s environment. The key is knowing your exposure and positioning accordingly.