One thing I don’t like about the rent versus buy debate (aside from how emotional and dogmatic it can get) is that it typically fails to factor in the existing real estate environment. The fact that we are in a seller’s market right now in the Boston area should influence your decision on whether to rent or buy, just like it would if deals were great in a buyer’s market.

I’m not saying that since inventory is tight and it’s hard to find good deals, buyers should give up and automatically rent. You might find something that works and there are non-financial reasons to own a home.

But if you find yourself chasing cash offers on homes going quick, or you aren’t sure you’re going to stay in the house for more than a few years, consider renting and waiting for the environment or your situation to change.

Greater Boston Seller’s Market

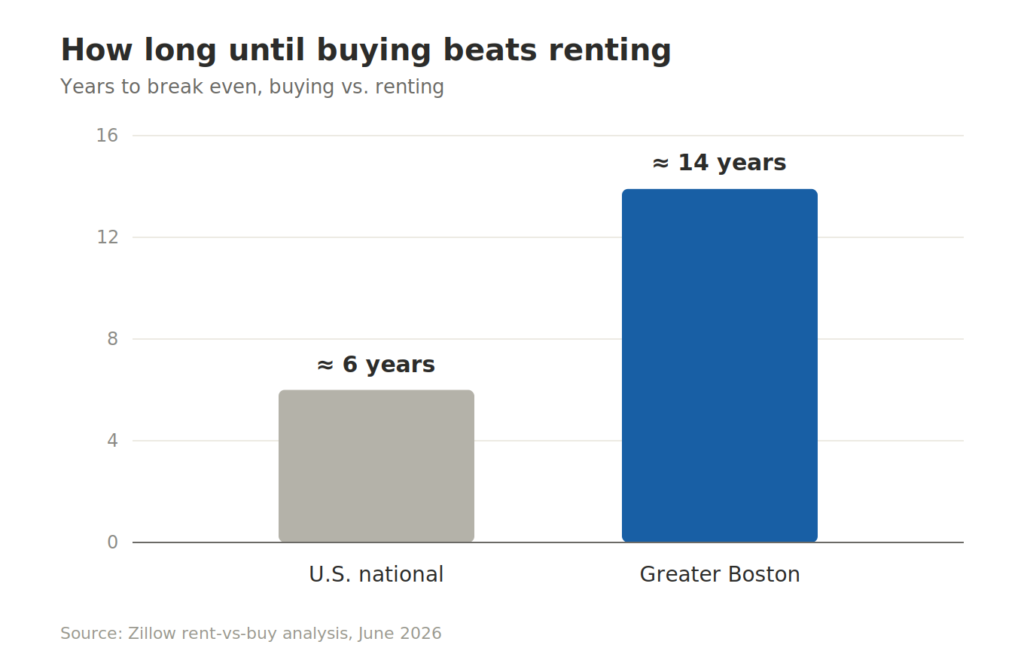

Zillow runs a breakeven analysis for every major metro — how long you’d need to own before buying beats renting, factoring the down payment, closing costs, taxes, insurance, maintenance, and eventual sale costs.

Nationally, that breakeven is about six years. In Boston it’s almost fourteen.

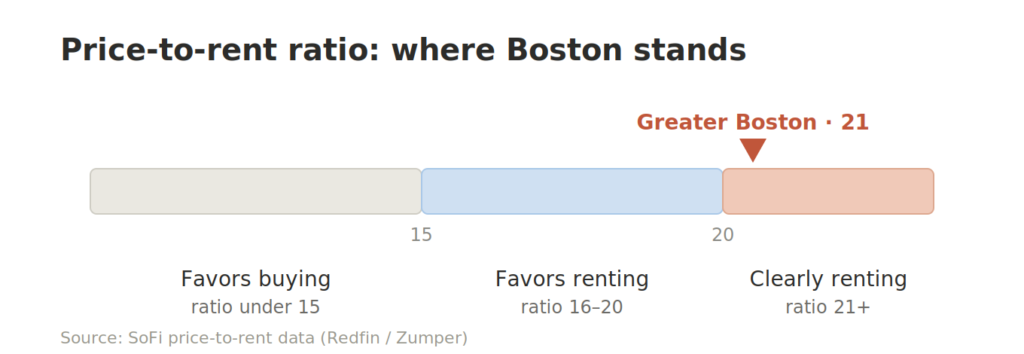

The price-to-rent ratio tells the same story. Price-to-rent is the median home price divided by the annual rent on a comparable home. It helps gauge how expensive buying is versus renting.

Boston comes in at about 21 according to SoFi. A ratio under 15 favors buying, 16 to 20 favors renting, and anything 21 or higher means makes renting the clear choice.

Renting Isn’t Throwing Money Away

OK, so you’re convinced that it’s a tough buyer’s market right now, but I can hear the objections – isn’t rent just throwing money away?

Rent isn’t wasting money. It’s paying a fair price for shelter. Throwing money away is walking to a trash can and dropping $20 bills in it. Try it out and see the difference. Just let me know where the trash can is first.

The Tax Break Isn’t What It Used To Be

Another thing to consider are the tax rules in place, since homeownership tax breaks (deducting your mortgage interest and property taxes from your income) have always been touted as a home buying benefit. However, recent tax law changes have somewhat negated these benefits.

The higher standard deduction in 2018 makes it so you only get a tax break from mortgage interest and property taxes if all your itemized deductions are higher than the standard number. Many buying starter homes end up taking the standard deduction.

For higher net worth individuals, it’s also a different story these days. There’s a limit on how much state and local tax you can deduct, which impacts people in states like Massachusetts harder.

The cap was raised for a few years, but it starts to phase out once your income gets above a certain level, and is scheduled to drop back down again later.

Homeownership Builds Wealth

It is true that home buying helps build wealth. Long-term research from Harvard’s Joint Center for Housing Studies shows that families who buy and stay owners see meaningful median wealth gains over time, even across boom and bust.

That wealth comes mostly from forced savings as mortgage payments reduce the principal owed. There’s also home price appreciation, but it’s probably less than you think. Robert Shiller’s home-price data shows real estate has delivered lower than 1% real returns annually.

But your parents bought a house thirty years ago for $250,000 with 20% down and just sold it for $730,000. That’s nearly three times their money. What do I mean home prices don’t go up?

Yes, but over thirty years that’s only a 3.6% annual return on the price appreciation. It’s almost 10 times the downpayment, which makes for an 8.2% annual return on that outlay. However, don’t forget the property taxes, insurance, mortgage payments, and maintenance they did on the home for thirty years. Those annual costs are likely more than what their rent would have been and eat most, if not all, the appreciation.

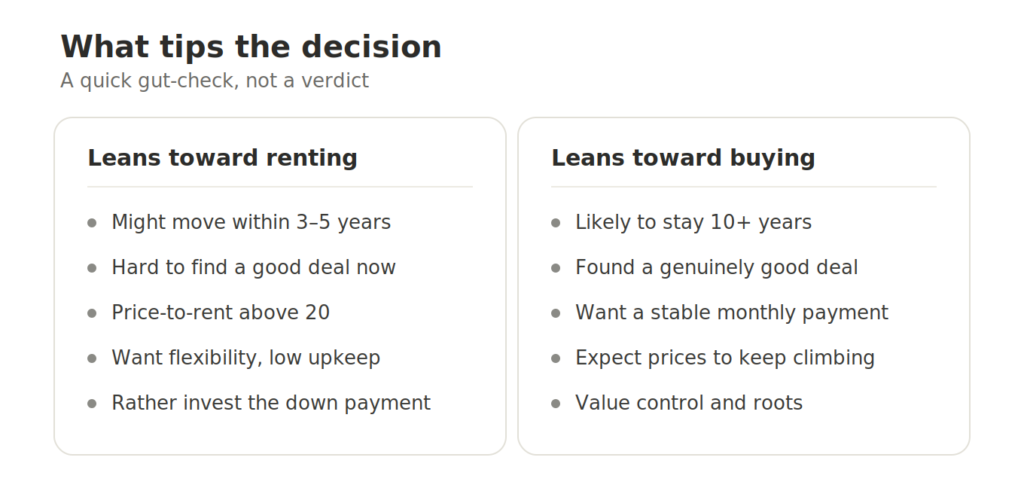

When Buying Still Wins

Buying a home carries advantages spreadsheets don’t capture, such as controlling your own space, building community roots, and the security that a landlord can’t sell out from under you.

As my frequent co-host on Your Money This Week says, you can get too caught up in the numbers. If you want the house, can afford it, and will own it for along time, go for it.

Beyond this, there are reasons to buy even now:

- You have a long time horizon which puts the breakeven math in your favor.

- It’s a good deal.

- You get payment stability. A fixed-rate mortgage locks your biggest monthly expense for thirty years, which is a real hedge as rents climb, even if taxes, insurance, and upkeep drift up.

- Prices could keep climbing. If Boston home values and rents don’t cool, buying sooner beats waiting, but we’d need a crystal ball for that one.

Final Thoughts on Rent vs. Buy in Boston

If you want to run your own numbers, there are good rent-vs-buy calculators out there. The New York Times and Zillow calculators are popular.

Just check two assumptions first. Make sure it isn’t crediting you the mortgage-interest and property-tax deductions if you’re going to take the standard deduction, and check the return it uses on the money you’d invest instead of buying. If it’s too low, it unreasonably tilts the answer toward owning.

Related Reads

Worrying About Residential Real Estate

A Young Reader Asks, Should I Start Investing in Real Estate?