Something I’ve been thinking about lately is whether we should be worrying about inflation. It’s a new topic, since inflation has been more bogeyman than anything during my career. Inflation fears have caused investment mistakes and bad economic policies. However, the Fed is targeting higher inflation, and there are other inflationary forces brewing, so we should take a closer look at the reasons for worrying about inflation, whether we should be worried, and if so, how to protect your portfolio from inflation risk.

Reasons for Worrying About Inflation

Inflation is the increase in goods and services prices. When things get more expensive, your earnings lose purchasing power, your cash is less valuable, and it’s harder to maintain your standard of living during retirement.

If a saved dollar earns .5% interest and inflation is 2.5%, every year that dollar loses 2% of its purchasing power. It might not seem like much, but over years it adds up. Between 1999-2019 a dollar lost 35% of its purchasing power during a period of below average inflation. Between 1970 and 1990 a dollar lost 70% of its purchasing power!

Inflation erodes purchasing power. Without it, a $1,125,000 nest egg that earns 8% per year could support annual spending of $100,000 for 30 years. If you assume 3% inflation, that nest egg only lasts you 17 years. With 5% inflation, your nest egg is gone after just 14 years.

The long-term inflation rate has been just over 3%. For the last twenty years, it’s been much lower at 2%, and for the last ten even lower than this at 1.75%.

When people talk about worrying about inflation, they’re talking about (or should be) inflation running hotter than it has recently, or its long-term average.

Inflation’s Negative Impact to Markets and Economy

Besides the hit to your finances, above average inflation impacts the markets and economy. To combat it, the Fed raises interest rates to slow the economy down. Higher interest rates makes borrowing more expensive. It makes real estate less affordable. Bond yields would increase, so stocks would not look as attractive as they do now when bonds yield very little. Dr. Ed’s quote sums it up well.

“If inflation were to make a big comeback, bond yields would soar. That could cause a credit crunch, recession, and a bear market.”

Dr. Ed Yardeni, Inflation Is Up for Discussion

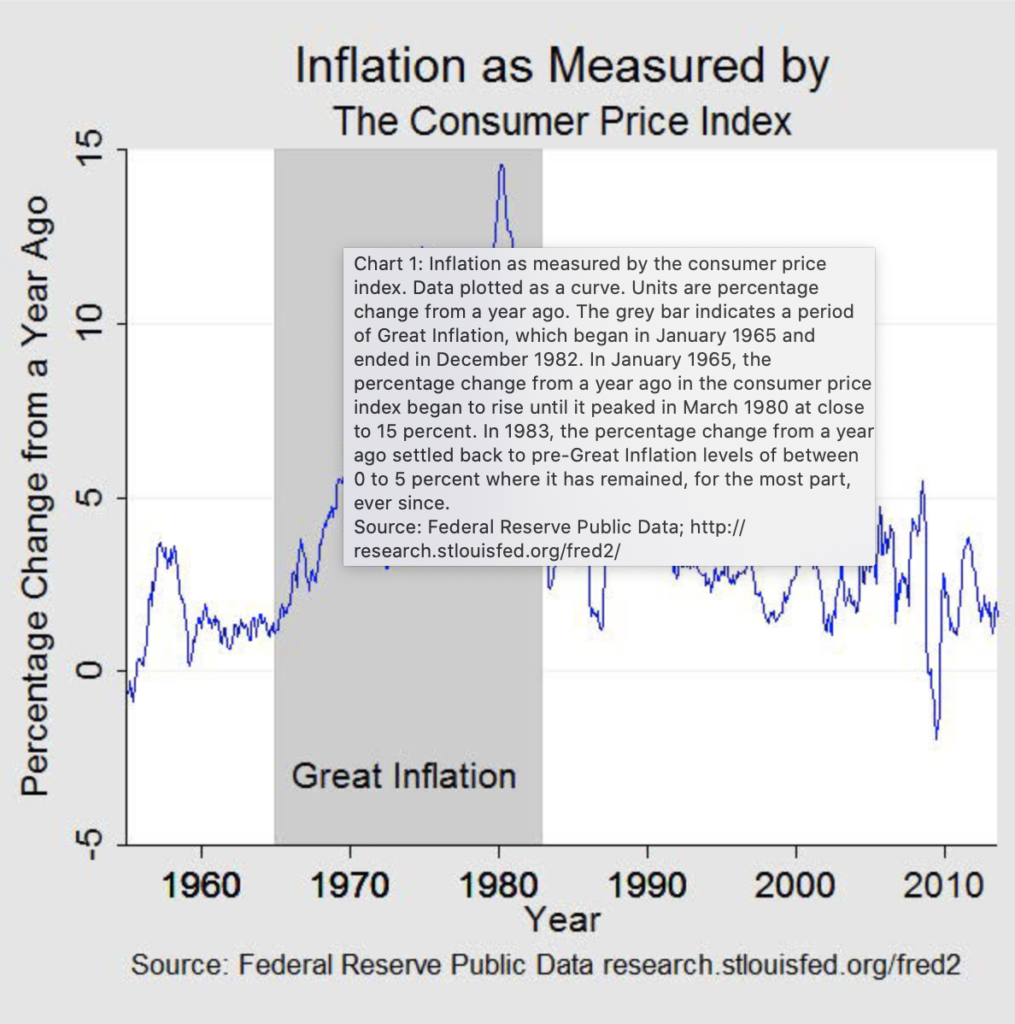

The country faced this between 1965 and 1982, and it’s worth reviewing that time period as we decide whether we should be worrying about inflation.

The “Great Inflation”

The Great Inflation was the defining macroeconomic event of the second half of the twentieth century. Over the nearly two decades it lasted, the global monetary system established during World War II was abandoned, there were four economic recessions, two severe energy shortages, and the unprecedented peacetime implementation of wage and price controls. It was, according to one prominent economist, “the greatest failure of American macroeconomic policy in the postwar period” (Siegel 1994).

The Great Inflation by Michael Bryan, Federal Reserve Bank of Atlanta

Inflation jumped from 1% in the early 60s to a peak of 14% caused mostly by government policy.

The Fed, in pursuing its dual mandate of maximum employment and controlling inflation, came to believe in the Phillips Curve, which held that there was a relationship between unemployment and inflation. Specifically, that above average inflation could permanently increase employment. The Philips curve proved unstable and drove inflation higher.

We went off the gold standard in the 1970s. While this benefited us long-term, at the time it allowed us to print money, which grew the economy but contributed to the Great Inflation.

LBJ’s Great Society and the Vietnam War drove up government spending.

Nixon’s wage price controls held inflation in check, but artificially so and when the controls were lifted, inflation shot up.

That, plus some oil and food shocks in the 70’s led to that chart you see above.

Reasons to Worry

There are reasons to be worrying about inflation.

For starters, the Federal Reserve in its 2020 Statement on Longer-Run Goals and Monetary Policy Strategy announced that, “following periods when inflation has been running persistently below 2 percent, appropriate monetary policy will likely aim to achieve inflation moderately above 2 percent for some time.”

They’re going to let inflation run above 2% to get to a long-term average of 2%.

Also, the economy is recovering, and certain tailwinds could cause it to overheat.

- Pent-up demand when the world fully reopens after Covid-19

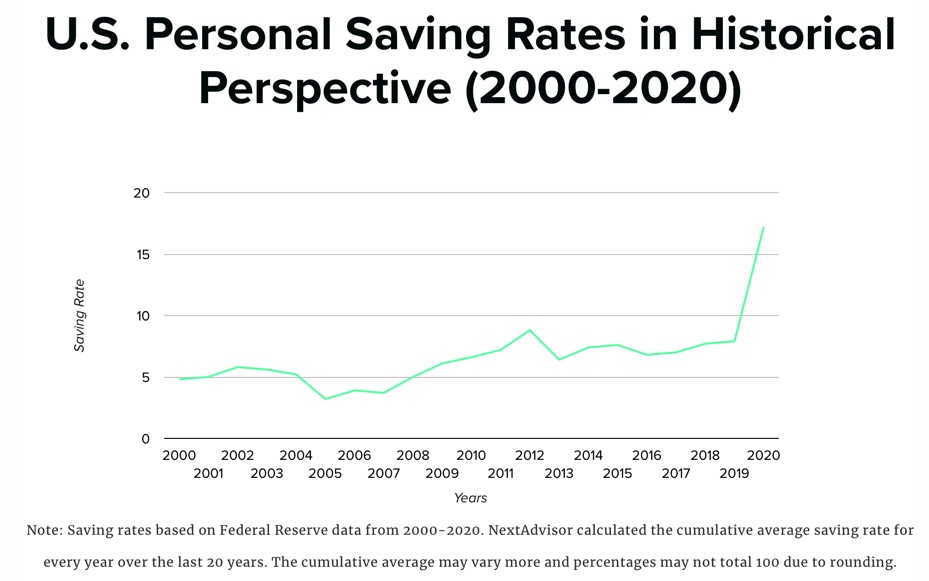

- Healthier personal balance sheets because the U.S. savings rate increased last year

- The Fed’s easy money policy

- President Biden’s expected $1.9 trillion Covid-10 relief bill

- Another further stimulus package

- The government stimulus enacted last year

And finally, those who fear inflation can point to what has caused it historically and draw parallels to today. In his book, Stocks for the Long Run, Jeremy Siegel points out that we didn’t see inflation for the 150 years leading up to World War Two. The gold standard held prices in check. However, it also limited the government’s ability to help the economy during crises by providing liquidity. With that ability to help came inflation.

No sustained inflation is possible without continuous money creation.

Stocks for The Long Run, Jeremy Siegel

And we have had plenty of money creation since the Great Financial Crisis.

Reasons Not to Worry

There are also good reasons for not worrying about inflation.

First, the bogeyman. People love to worry needlessly about inflation. We’ve seen just one time period where higher inflation was an issue in the last few decades. We’ve seen many harmful false alarms. Most recently, the Fed was worried about inflation well into 2008 and decided as late as September of that year not to cut rates even further in the midst of a credit crisis because of inflation worries. How the Fed Let the World Blow up in 2008 chronicles that story well.

Second, an aging global population, globalization, and technology are three deflationary forces keeping prices in check.

Third, the money printing since 2008 hasn’t sparked inflation.

Fourth, as we discussed above, the “Great Inflation” was caused by a few things, not simply an increase in money supply and government spending. One was a Fed mistake that they have learned from to our benefit.

But that failure [of American macroeconomic policy] also brought a transformative change in macroeconomic theory and, ultimately, the rules that today guide the monetary policies of the Federal Reserve and other central banks around the world.

The Great Inflation by Michael Bryan, Federal Reserve Bank of Atlanta

What Should You Do

Reasons exist for worrying about higher inflation. There are also reasons not to worry about it.

My two cents: it’s reasonable to assume that inflation will run hotter than it has given the Fed’s statements. And, we have seen that central bankers and economists, while well intentioned, can make mistakes. Are we certain they can stick the inflation landing perfectly, dialing up inflation a bit and then dialing it back down? Perhaps, but I’m skeptical.

And throwing stimulus into a recovering economy that will also benefit when bored Americans unleash their savings should be inflationary.

But that does not mean that we are going back to the 60’s and 70’s. For one thing, the clothes and wood-paneled station wagons wouldn’t fly today. High inflation is a rarity, and many strange things combined to create it the last time around.

So, I would expect it, but wouldn’t overreact to the possibility.

Preparing Your Portfolio

To prepare your portfolio, I’d consider the following.

- Reduce long-term bonds. Long-term bonds should decrease in value more when interest rates rise than short-term bonds. Higher inflation should cause rates to rise as the yield curve steepens. Owning short-term bonds provides almost as much return, stronger protection from rising rates, and the ability to more easily reposition your portfolio into longer-term bonds when the yield curve steepens.

- Increase stock exposure. Low-yielding bonds and cash will lose purchasing power if inflation picks up. Stocks may not perform well when inflation initially picks up, but they are great long-term ways to maintain purchasing power. Increased stock exposure comes with increased risk, but, if you have been underweight stocks it’s time to consider buying some. The exact amount depends on your financial plan and risk tolerance.

- Add real assets exposure. Real assets include real estate, land, infrastructure, timber, and commodities. They have historically done well in inflationary environments. There are challenges when investing in commodities through products that use futures contracts, and gold increases in value because people expect it to during times of economic stress, but price-conscious investors can’t value it. Consider shifting some of your bond allocation to real assets, but be careful with gold and commodities.

- Rebalance your portfolio. Higher inflation will likely cause the Fed to raise rates to slow the economy down. This will hurt stocks. You won’t be able to time this, and don’t need to. But, rebalance and take stock profits as the bull market continues to ensure that you are not over-exposed to stocks if we get a major pullback.

Suggested Further Reading:

Why to Watch (and not fight) the Fed – The Fed moves markets, particularly since 2008. Understand why, what to watch for now in the inflation debate, how the Fed might react, and what that means for your portfolio.

Thoughts on Our Team’s 2021 Investment Outlook – Our 2021 investment outlook is an in-depth look at investment themes that will matter this year and how to position your portfolio well to take advantage. It’s worth the full read, and here are my thoughts.